Author: Zhi Wu Bu Yan

Around 2006, a group of small foreign trade bosses in Guangdong and Fujian began exploring opening stores on eBay. They sat in small offices next to factories, using broken English to do business with strangers on the other side of the globe.

The hardest part wasn't the language, nor the logistics, but the money—how to get an American buyer to safely transfer money to a Chinese seller?

What made this possible was a blue button. That button was called PayPal.

At that time, PayPal represented the forefront of financial democratization and the most advanced productivity. Following the "Website Payments Standard Integration Guide," global small merchants only needed to input a piece of HTML code on their web pages to receive payments worldwide.

This technological flattening, combined with being the only officially recommended payment method during the eBay era, made PayPal the undisputed global payment hegemon. Even today, when you open any overseas checkout page, PayPal will definitely have a place.

Twenty years have passed. Many of those small foreign trade bosses have grown from eBay shops into independent sites, Amazon stores, TikTok, and Temu-flourishing cross-border merchants. China's cross-border e-commerce export scale has exceeded 2 trillion RMB, and payment tools have blossomed from a single blue button into Stripe, Wise, LianLian, and Wanlihui's hundred flowers blooming together.

This industry has grown up, but PayPal has somewhat fallen behind.

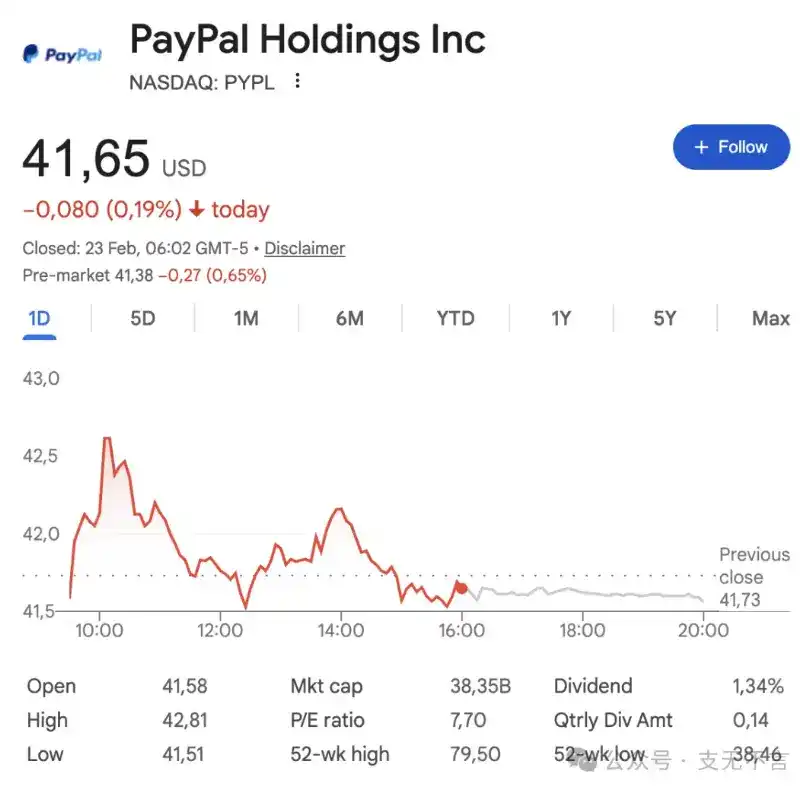

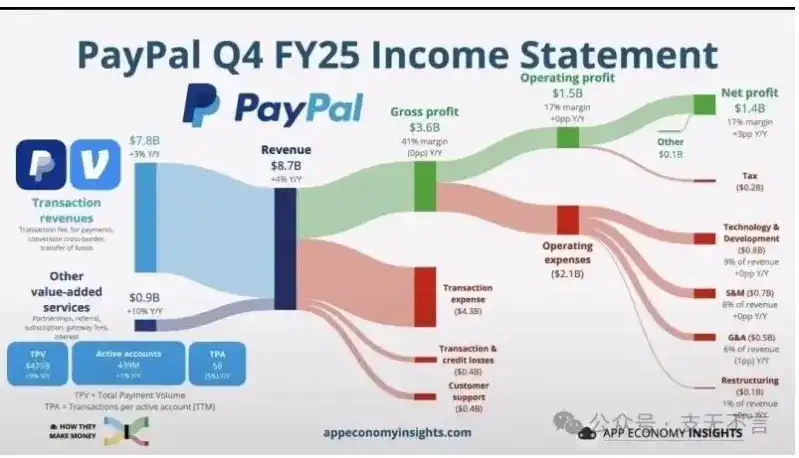

Three weeks ago, on February 3rd, PayPal announced its financial report, with its single-day stock price plunging 20%, and the CEO resigned abruptly. The main source of profit, branded checkout, saw its active user growth rate drop from the once high-speed track to 1%, and the transaction volume of active accounts decreased by 5% over the past 12 months.

Whether it's Stripe's one-link payment, Apple Pay with biometric verification, or even just using Google to fill in bank card information, it all seems more convenient than that slightly outdated blue icon interface that might require remembering a login password.

It was once a legend co-created by people like Musk, Peter Thiel, and Hoffman. Persson once held it heavily, and Muji was its most loyal supporter, but they all chose to clear their positions.

PayPal's market value has fallen from its pandemic peak of $363 billion to a recent new low of $38 billion—evaporating 90% in five years, with the P/E ratio touching as low as 7.4. It wasn't until Bloomberg's exclusive today that at least one large competitor is evaluating an overall acquisition, with multiple parties expressing interest in some assets, that the stock price rose nearly 10%.

This news itself is the most precise footnote to PayPal's situation. When a company starts to be seen as prey rather than a hunter, and its market value rises because of it, it shows that the market's confidence in its independent operation is lower than the expectation of it being bought out.

The former payment empire, like the aging British Empire, still has its flags planted around the world, the sun hasn't set yet, but those who see it no longer have the awe they once did. Everyone knows in their hearts that the era has changed. But how did it decline?

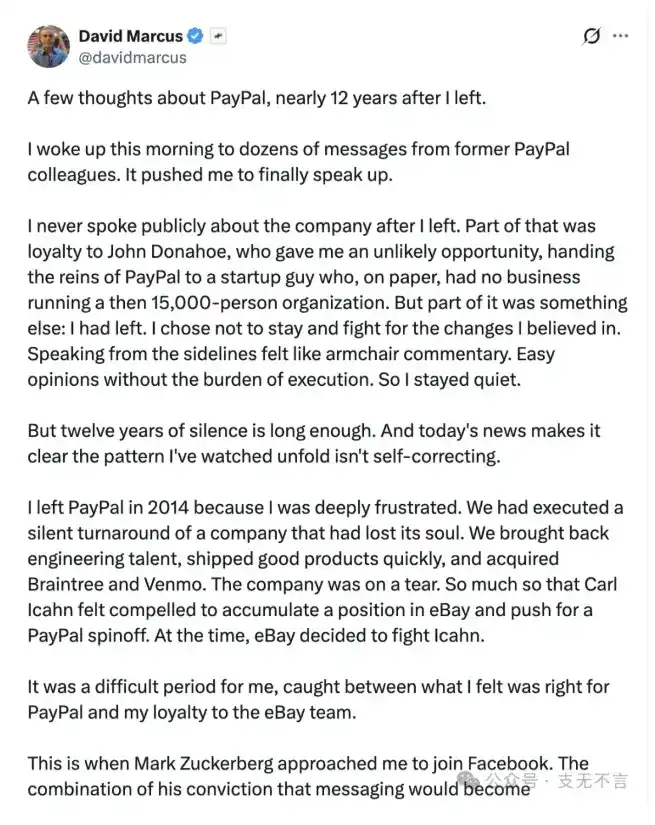

"It's really painful to see a company I love so much come to this point."

On February 3rd, former PayPal CEO David Marcus posted a long article on X, rarely fiercely criticizing this company he once devoted his heart and soul to.

David Marcus's career has always been accompanied by radical financial innovation. He currently serves as the CEO of Lightning Network payment company LightSpark. During his time at PayPal, he recruited top engineering talent and led the acquisitions of Braintree and Venmo; during his time at Facebook, he was one of the leaders of the once sensational stablecoin project Libra. Although Libra foundered due to regulatory reasons, today's stablecoin热潮 is enough to prove David's foresight and boldness.

Besides the stock price plunge, another reason that stimulated David to post this long thread was that the former CEO Alex Chriss resigned after less than three years in office, replaced by former HP CEO Enrique Lores.

Enrique Lores served as HP's CEO for 7 years, launched the money-making model of printing as a service, and initiated large-scale layoff plans—undoubtedly a master of cost reduction, efficiency improvement, and business restructuring. And if PayPal's board had already considered selling the whole or parts of PayPal, this choice seems even more reasonable.

David expressed his dissatisfaction implicitly: "I don't know Enrique. He might be a great leader, but at least based on paper information, he is a hardware industry executive who has now parachuted into a payment company."

This echoes David's core criticism. Unlike the market voting with its feet due to poor financial performance, David believes PayPal's fate lies in—"the company's leadership style has completely shifted from 'product-driven' to 'finance-driven.' Over time, belief in product gave way to financial optimization."

Quoting a famous saying by Benjamin Franklin: Any company that sacrifices product for short-term stock performance will eventually fall behind the tide of the product era and lose its stock price.

David believes PayPal has lost its "mojo."This was a spirit during PayPal's early days, that wild power daring to turn the office upside down to solve an impossible problem. But today, this power has been replaced by compliance reviews and financial optimization.

Stripe, which conquered developers with its concise API, has this mojo. Opening Stripe, that constantly bouncing "Global GDP running on Stripe" in the top left corner is a conqueror's quality.

Apple Pay, which has been vigorously pushing Passkey in recent years, has this mojo. Relying on underlying security chips and Face ID, it has made the payment experience extremely comfortable—lift wrist, scan face, done, without even opening the App. This is something PayPal, which still stays on jump pages, re-authorization, and waiting for confirmation three-step experience, cannot match.

Revolut, representing Neobank, has this mojo. With strong execution, this emerging enterprise quickly opened a full-stack financial platform covering stocks, foreign exchange, and cryptocurrencies in dozens of countries in a very short time, and is constantly expanding its territory.

These three companies have a common point: their mojo doesn't come from scale, nor from user numbers, nor even from money. They come from a product belief: believing that what they are doing will make a corner of the world different.

And this is just the tip of the iceberg. Shop Pay, Klarna, Affirm, afterpay, Wise, Cash App, Adyen—every niche in the payment track is crowded with people.

PayPal once had this thing too. That piece of HTML code, that button that enabled cross-border settlement between an American uncle selling second-hand goods in a garage and a small factory boss doing foreign trade in Guangzhou, was itself a declaration of changing the world. But the process of losing it was quiet, almost silent.

Mentioning PayPal's development in recent years, one must mention Venmo.

Venmo did one thing right: it made transfers social—splitting meal money, AA paying rent, sending it to friends with an emoji, much more fun than bank transfers. The way it spread among American young people was more like a social software than a payment tool. "Venmo me" even became a verb, a synonym for transfers among American youth.

PayPal's acquisition of Venmo was actually a byproduct of acquiring payment service provider Braintree. This product, which wasn't very eye-catching at the time, is now a bright spot in PayPal's暗淡 financial report: 2025 revenue of $1.7 billion, monthly active accounts breaking 100 million, Pay with Venmo transaction volume同比增长 50%, credit card users growing 40%.

But behind these numbers, several deep-seated issues are fermenting: those who are optimistic about it are obsessed with the doubled credit card transaction volume, believing this cash cow is entering a monetized harvest period; while those who worry about it will反问, if this prosperity is just fishing in the remaining存量 social circle, how long can this afterglow last?

This rift essentially reflects Venmo's陷入生态位的夹击中:向上, it hits the hard walls built by Apple Pay and Google Pay;向下, it can't drill into the underlying pipelines deeply embedded by Stripe and Adyen. Venmo's growth is strong, but the ceiling is also obvious.

First is the internal consumption of the growth model. Behind the 20% revenue growth rate is only a 7% active user growth—Venmo is no longer expanding territory, but taxing its own people, squeezing the same batch of users more fully, but failing to attract a new generation to come in.

其次是地理与产品灵魂的双重困局。Venmo始终被锁定在美国本土,抓住了美国的餐桌,却还远远没有走进世界的收银台。

最后是全场景金融想象的暂时落空。PayPal为Venmo设计的商业闭环里,还有一个叫Honey的购物插件,本来是要打通"发现-结算"链路的。但2024年Honey因篡改联盟链接的丑闻几乎崩盘,这根导流管断了,Venmo的蜕变之路也随之打了折扣。

一个独立的消费者支付应用,如何证明自己值得用户主动打开?这个问题,Venmo正在努力回答,但 the answer has not yet been revealed.

Venmo折射的是PayPal在消费者侧的考量。在更远的前沿,PayPal还押注了另外两张牌—一个叫 PYUSD,一个叫 Agent支付。这两张牌的共性是:赛道足够大,但胜算都还没有着落。

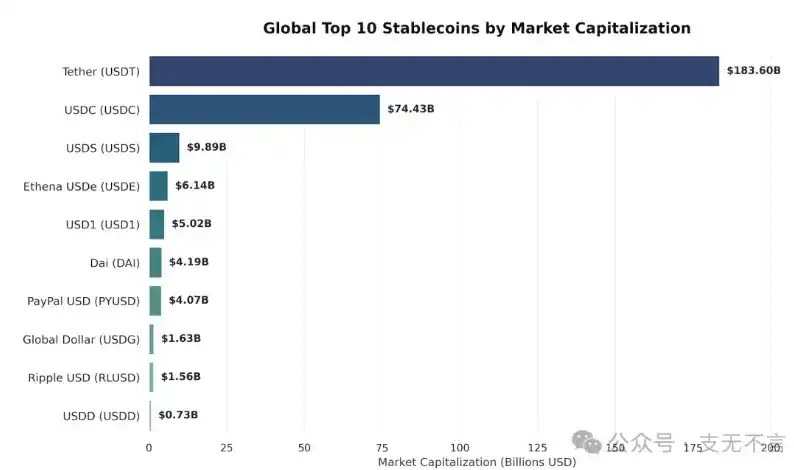

Objectively speaking, PYUSD isn't done poorly. Since its release in 2023, the market scale has reached $4 billion, ranking in the top ten of global stablecoin market value. But compared to Tether's约 $180 billion USDT and Circle's约 $70 billion USDC, PYUSD's volume can only be called a fraction.

It反而证明了一件事:even if everyone can issue stablecoins, the barriers of channel distribution and user心智 are still very high; a behemoth like PayPal cannot指望降维打击.

When PayPal announced in April 2025 that it would give PYUSD holders a 4% annual interest rate, the industry一度惊呼巨头要杀死比赛了,然而事物发展是渐进的。Stablecoins' current trillion-level usage mainly comes from crypto trading对冲搬砖和做市,跨境套利和灰产资金转移,DeFi 借贷、LP、yield farming 的基础资产,这些并非PYUSD所长。

未来稳定币的使用场景当然会越来越阳光化和日常化,跨境B2B支付、链上结算、日常零售,但竞争也是极其激烈的,且不说USDT和USDC两座大山,创新导向的USDe和背靠特普家族的USD1都是劲敌,PYUSD并没有什么十足的胜算。

Besides stablecoins, PayPal has also set its sights on agentic payment. They abandoned the error-prone web crawler,转而与商家订单管理系统进行API对接。商家只需签署协议,PayPal就能将他们的库存、颜色、价格等实时数据,分发到 Google Gemini等主流 AI 平台,以及 PayPal 自身的 App 中。

The思路是清晰的,但这是一个待验证的市场,最近千问撒红包请大家喝奶茶,算是给国内的消费者来了一次AI购物的市场教育,但改变消费者习惯绝非一朝一夕,和AI聊天来购物是否会成为主流,还是说购物的主力体验就在于一个人慢慢挑货比三家, still an unknown number.

即使未来人们真的习惯了 saying to ChatGPT: "Help me buy a cup of 去冰三分甜乌龙茶," those掌控交易留存数据的,仍然是拥有海量用户的AI平台,这些AI平台还大概率拥有自己的生态支付手段,或是雨露均沾,在这个全新的链条里,PayPal的地位依旧存疑。

After talking about so many losses and uncertainties, you might feel that PayPal's story has already been written to its period.

But facts are never one-sided. Braintree is still the underlying payment framework for many global platforms. Pay Later processed over $40 billion in transaction volume in 2025, leading the US BNPL market share. The Fastlane one-click checkout launched in August '24 was one of its rare active出击,直接叫板Apple Pay和Shop Pay。加上4亿活跃账户、全年超$60亿自由现金流——these assets, in the eyes of any company wanting to position itself in the AI agent economy era, are strategic entry tickets难以从零复制.

The accumulation of nearly thirty years has not been in vain, nor will it disappear凭空。只是可惜,大江东去浪淘尽。

The person who best knows how to use this ticket may no longer be PayPal itself.